Gransino KYC Verification: Documents, Timing and Withdrawal Impact

Loading...

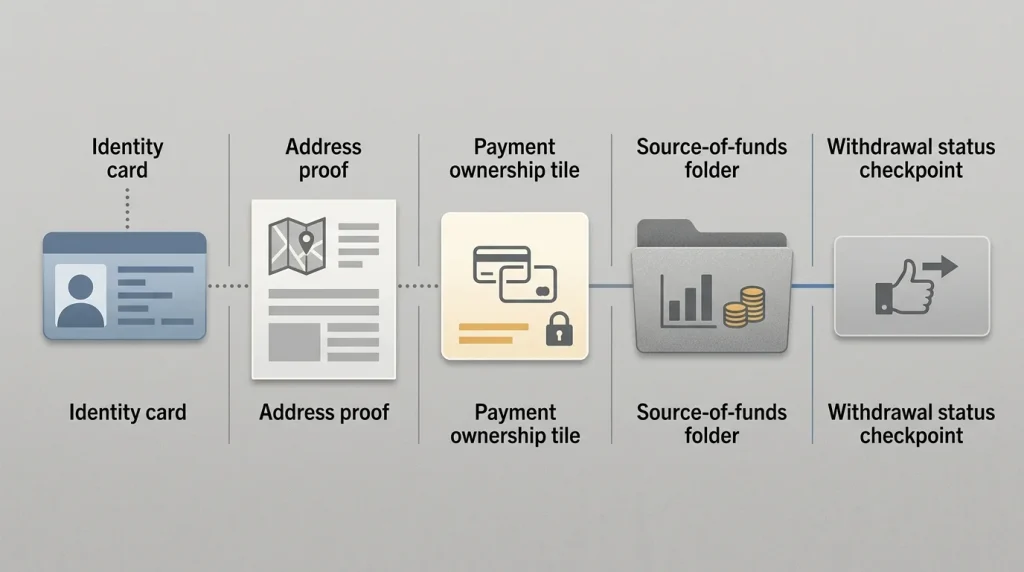

Gransino KYC verification can affect deposits, withdrawals and continued account use. The official General Terms say Gransino can request information to manage an account, verify identity, verify age, verify residence and verify the source of funds. The listed examples include certified ID, proof of residence, proof of payment-method ownership and transaction histories such as bank or card statements. Requested information must be provided within 30 days, and the terms say documents are usually verified within 10 days after a full response, with additional time or checks possible.

This page explains what that means for a UK-focused reader. It links to the main guide, the wider account guide, the withdrawal impact page, the payment checks page and the player-protection context. It does not promise no-KYC play, instant approval or guaranteed withdrawal timing.

What Gransino can ask to verify

The official terms give a clear framework for verification. Gransino can request information to manage the account, verify identity and verify the source of deposited funds. The same section refers to KYC checks both before and after deposits or withdrawals. That means verification is not only a registration issue. It can also appear later when the account has activity, balance, bonus use or a withdrawal request.

The official document examples are specific. They include properly certified ID, proof of residence, proof of ownership of payment methods used, and transaction histories of payment methods, including bank or credit or debit card statements. A separate refund-related section also gives examples such as passport, driving licence, identity card, utility bill, bank statement and rental agreement.

Those examples should not be expanded into an invented universal checklist. The exact request belongs to the account case. The review can state the sourced categories and explain why they matter, but it should not claim that every reader will need the same document or receive the same verification outcome.

Timing: 30-day response and usual 10-day verification

The official terms say requested documents and information must be provided within 30 days after the request is made. They also say Gransino will usually verify documents and information within 10 days after the request is answered in full. The same wording allows for additional time and additional checks depending on the circumstances and complexity of the case.

This is a high-risk fact because timing can affect a reader’s expectations around withdrawals. The safest public wording is exact and limited: 30 days to provide requested information, usually within 10 days after a full response for verification, with additional time or checks possible. Do not turn that into a fixed approval promise, a maximum waiting time or a guarantee that all account activity will continue during the review.

The phrase “answered in full” is important. A partial upload, unclear photo, mismatched address, unsupported payment method or missing bank statement can keep the request open. A reader should treat the clock as dependent on a complete response, not just on the first message received from support.

How KYC affects withdrawals

Withdrawal readiness depends on verification. The official terms say withdrawal requests are worked through by the financial department within 3 business days after the request is made, or within 3 business days after the last withdrawal request was paid out, provided the other conditions are met and checks are completed. The terms also say withdrawals can be delayed for checks of identity, account balance, source of funds and compliance with the terms.

That means the headline processing window is conditional. It sits behind account consistency, payment ownership, wagering or turnover conditions, bonus terms and KYC. The payout checks page covers withdrawal logic in more detail; this page focuses on the verification layer that can decide whether a withdrawal request is straightforward or stalled.

A reader should not deposit first and read verification rules later. Before relying on any withdrawal, check that account name, payment method, address and source-of-funds evidence can be supported if asked.

Payment ownership is part of verification

The terms connect account warranties with payment ownership. They say the credit or debit card or other payment method used to top up the account must belong to the account holder, must not be stolen and must not be lost by another person. The payment section also says withdrawals are processed using the same payment method used to fund the account wherever possible.

For UK readers, the practical point is simple: do not treat someone else’s card, wallet or bank account as a shortcut. It can create a verification problem later, even when a deposit looks successful. Payment ownership can also affect refunds, withdrawals, chargeback handling and support review.

The cashier evidence guide explains why payment-method availability should be checked inside the account. This KYC page adds the identity layer: the payment route should match the person, country details and documents behind the account.

Privacy and data categories

The official Privacy Notice lists registration data, due-diligence data and financial information that can be collected. Registration data includes personal details used to create an account. Due-diligence data includes identity document number, driving licence or passport number, proof of address, source of wealth or funds, bank ID and financial statements or details. Financial information can be used for deposits, withdrawals, KYC and AML compliance.

That privacy evidence supports the same decision guidance as the terms: KYC is not just a document upload. It is a data process involving identity, address, payment and source-of-funds information. A reader should avoid sending extra personal data outside the official process, but should be prepared for the official account flow to ask for data that matches the terms and privacy notice.

Keep copies of submitted documents, upload dates and support responses. Use secure storage and do not send unnecessary full document packs to unrelated review sites or social-media accounts.

What not to assume

Do not assume Gransino is a no-KYC casino. The official terms directly support KYC, source-of-funds and payment-ownership checks. Do not assume verification is instant. The terms give a usual verification timeframe after a full response and preserve room for additional checks. Do not assume a withdrawal processing window starts cleanly if KYC, payment ownership, bonus terms or account consistency remain unresolved.

Do not assume UKGC protection. The project did not verify a UKGC licence or a UKGC register hit for Gransino, and this page does not claim one. The absence of the United Kingdom from the general Excluded Jurisdictions list is not the same as regulated UK status or a personal eligibility decision.

Do not treat KYC as something to evade. If identity, address, age, residence or source-of-funds checks are requested, the safe action is to respond through the official process or stop using the account if the request cannot be completed.

Preparation checklist before depositing

- Use the official account details in your own correct name.

- Keep the address, date of birth, country and contact details consistent.

- Use only payment methods that belong to the account holder.

- Read the terms on verification before relying on withdrawals.

- Prepare clear evidence for identity, address and payment ownership if requested.

- Keep a record of upload dates and support replies.

- Do not open duplicate accounts after a verification or login problem.

- Do not seek instructions for bypassing KYC, account blocks or self-exclusion.

Support and escalation discipline

Gransino lists [email protected] in support, account and privacy contexts, and live chat support is verified. A verification issue should be handled through official support channels only. The message should include the account identifier requested by the official process, the issue summary, relevant dates and the document category being discussed.

Avoid sending unsupported claims such as “my withdrawal is guaranteed” or “verification must be finished today”. The sourced terms do not support those positions. A stronger message is factual: what was requested, what was provided, when it was provided and what response is needed next.

Bottom line on Gransino KYC

Gransino KYC should be read as a central account condition. The official terms support identity, age, residence, source-of-funds and payment-ownership checks. They also connect completed checks with withdrawal processing. The practical reader takeaway is to prepare before funding the account, not after a withdrawal has already become urgent.

A UK-focused review should be precise rather than dramatic. It can state the verified document categories, the 30-day response requirement and the usual 10-day verification wording after a full response. It should not promise instant withdrawals, no-KYC play, UKGC coverage or a fixed outcome for every account.

FAQ

What KYC categories are relevant to Gransino?

The reviewed terms support identity, age, residence, source-of-funds and payment-ownership checks. The exact request depends on the account case.

Does this page promise a fixed verification time?

No. It explains the sourced timing language and the practical effect on withdrawals, but it does not promise a fixed outcome for every reader.

Why does payment ownership matter?

Payment ownership helps the operator connect the account holder with the method used for deposits or withdrawals. Using another person"s method can create verification problems.

When should documents be prepared?

Before depositing is best. Waiting until a withdrawal is urgent can make account review, document quality and payment-method questions harder to manage calmly.

Gransino Account UK: Registration, Login, Mobile and Verification

Published by the Gransino Casino team.